By Ishac Diwan

Saturday, September 4, 2021 |

|

|---|

|

The collapsing economy is bringing misery now apparent in every day's life. To comprehend its scale, it is necessary to look at macroeconomic data. Recent data released by the World Bank and the Central Bank of Lebanon (BDL) provide estimates of the national and external accounts for 2020. These accounts make apparent two specificities of the crisis: A collapse in production, and an explosion of capital flight. These phenomena are related, and unless reversed, misery can only rise.

|

|

|---|

|

Capital flows and domestic production

The proximate cause of Lebanon's disaster is by now clear: A country over-spending on credit, without a commensurate rise in production, followed by a sudden stop of financial inflows when trust in a soft landing evaporated. External inflows were $13 billion in 2018, allowing for a high, but unsustainable level of aggregate spending. By the end of 2020, less than $4 billion tickled in.

The challenge faced by countries subjected to such an economic shock is that initially, domestic production falls as well. With consumer demand down, firms have to shift their production towards exports, and this takes time, allowing for destruction to occur prior to creation.

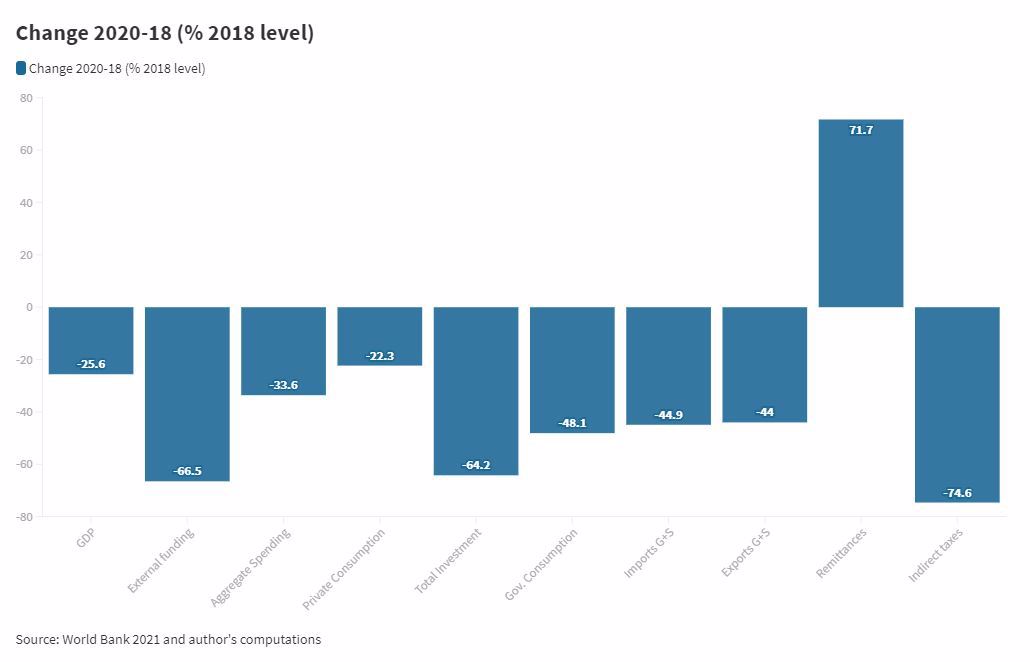

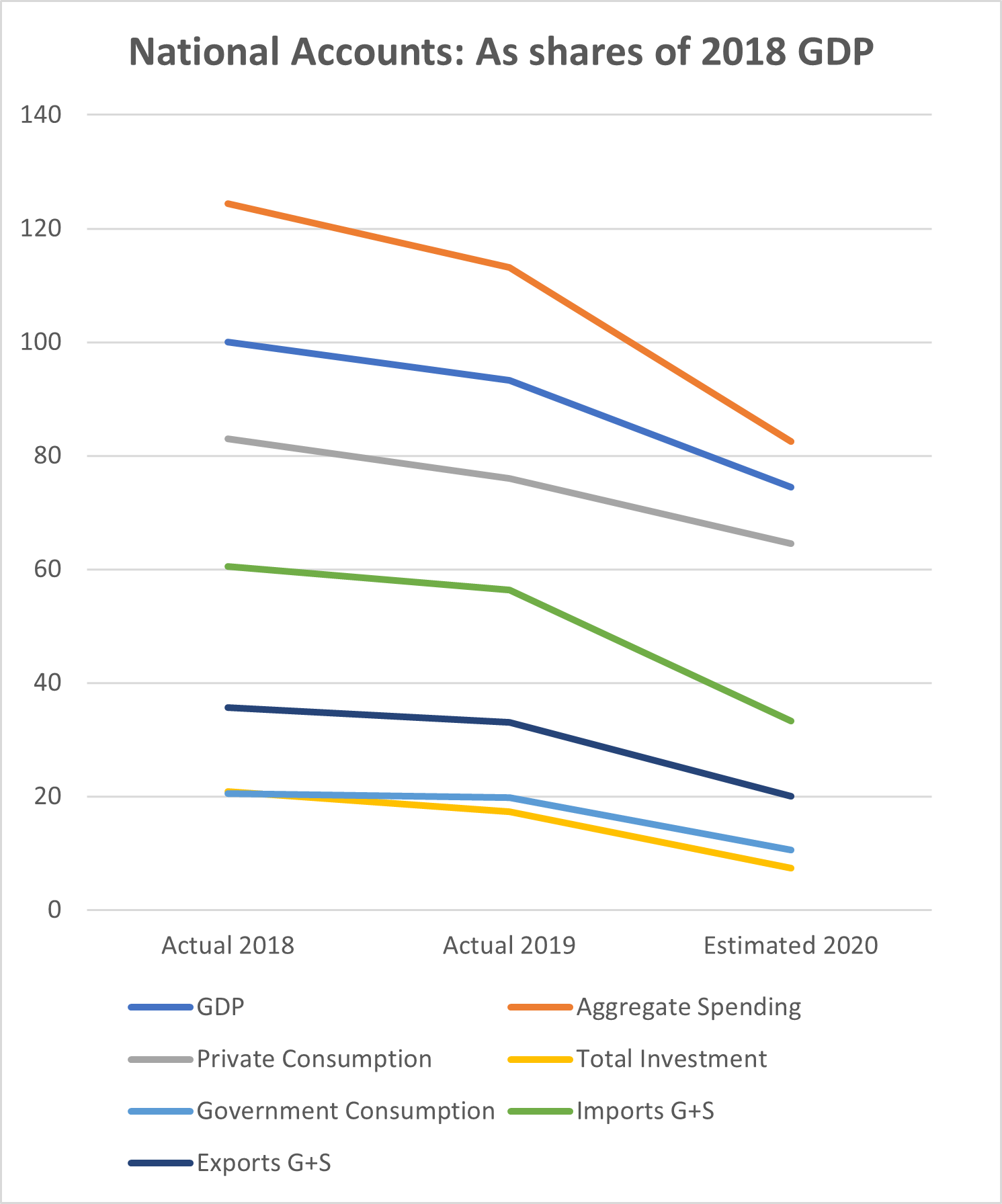

The first specificity of Lebanon is that production collapsed. By the end of 2021, GDP is expected to decrease by 40% relative to its 2018 level, making the shock much more severe. As a result, expenditures are also expected to collapse. According to World Bank data, in 2020 national expenditures were a third lower than in 2018, with investment down by 64% and government spending by 48%. Private consumption fell by 22%. These trends will worsen in 2021, especially for consumption, as subsidies financed by reserves, which accounted for half of 2020 imports, are being eliminated.

|

|

|---|

|

"The reason for the production collapse is the huge collateral damage done by misguided policies."

|

|

|---|

|

The reason for the production collapse is the huge collateral damage done by misguided policies. Three main mechanisms initiate a rebound: a devaluation of the exchange rate, which makes exports more attractive; an effective credit market, that allows firms to adjust their production structure; and counter-cyclical monetary and fiscal policies, supported by foreign funding, that ease the pain and re-establish macro stability.

Despite a huge devaluation, the utter destruction brought to the banking, fiscal, and monetary institutions by disastrous policies have ended up deepening the crisis. In the absence of credit, power, and price stability, it will be impossible for output to recover. Too many firms are going bankrupt, including those that should lead a recovery. Instead of rising, exports of goods and services were actually cut in half in 2020.

|

|

|---|

|

"The first specificity of Lebanon is that production collapsed. By the end of 2021, GDP is expected to decrease by 40% relative to its 2018 level, making the shock much more severe."

|

|

|---|

|

A sinking ship

There is also, unfortunately, more pain to come. After two years of crisis, the rebuilding of the economy has not even begun. The production collapse has occurred even before energy subsidies have been removed, fiscal and monetary policies have started to adjust, and banks have been cleaned up. All these policies are necessary for a rebound, but initially, they will hurt firms even more as energy prices and taxes rise, liquidity becomes scarcer, and losses in bank deposits get confirmed.

The expectation that policies will not improve aggravates the crisis, creating a vicious circle. The exodus of the youth and professionals is bleeding the country's human capital. But equally, capital is also leaving, instead of investing in a new growth path. The accelerated expansion of money supply is breading hyperinflation. This, and the loss of access to bank savings, is pushing the middle class to accumulate scarce dollars. Meanwhile, the influential rich with political connections and access to BDL reserves have been sending their deposits abroad to avoid future haircuts.

|

|

|---|

|

"The collapse in production amidst capital and skills flight illuminate the real causes of the crisis: A dead rentier economic model that is unable to transition to a productive one; and deeper down, a failed political system that is unable to advance the public good."

|

|

|---|

|

The external accounts recently published by BDL reveal the enormity of capital flight, the second specificity of the crisis. Paradoxically, more dollars were pumped in the economy by BDL in 2020 than flowed voluntarily in before the crisis. Of the $14.2 billion of official reserves it spent (during the first 3 quarters of 2020), more than $10 billion are now in either in banks abroad or hidden under mattresses. This flight to dollars is making imports ever more expensive: during 2020, inflation was about 80%, but the LBP fell from 1500 to 8000 to the dollar, implying a 3-folds real devaluation. As a result, the capital goods necessary for investment have become unaffordable, and consumption will shrink further in 2021.

Which Policies?

The collapse in production amidst capital and skills flight illuminate the real causes of the crisis: A dead rentier economic model that is unable to transition to a productive one; and deeper down, a failed political system that is unable to advance the public good.

It will not be possible for limited reforms to initiate a recovery. Eliminating subsidies will save on remaining BDL reserves. But a social safety net cannot be funded for long unless taxes are increased, or foreign funding becomes available. However, both are predicated on comprehensive reforms. Partial fixes, as we have witnessed so far, only signal that the reforms needed to stabilize and increase production continue to be avoided, that capital and people will continue to rush to the exits, deepening the crisis even more.

|

|

|---|

|

References

World Bank. Lebanon Sinking. Spring 2021. Table 4 (Selected Macroeconomic Indicators, 2016-2021)

Banque du Liban: Quarterly Bulletin, 4th quarter, 2020. Table 6.1 (Balance of Payments)

|

|

|---|

|

Ishac Diwan, PhD, Professor of Economics at Paris Sciences et Lettres (a consortium of Parisian universities) and Chair Socio-Economy of the Arab World, Professor of Economics at the École normale supérieure in Paris, Senior Fellow at the Issam Fares Institute for Public Policy and International Affairs (IFI) at the American University of Beirut (AUB)

|

|

|---|

|

While Lebanon is facing a total collapse scenario due to an unprecedented economic crisis, IFI launched an OpEd series that tackles the drastic repercussions of the crisis on the state's sectors and the people's living conditions.

The series will cover several facets of the crisis, pertaining to education, energy, economy, public health, and the private sector, in addition to human rights protection, gender equality among others.

|

|

|---|

|

Opinions expressed in these articles are those of the author and do not necessarily reflect the views of the Issam Fares Institute for Public Policy and International Affairs at the American University of Beirut.

|

|

|---|

|

|